How Are Diamonds Made? Natural vs Lab-Created Explained

Two Paths, One Diamond Not all diamonds come from the same place — but they all start the same way. Pure carbon, crystalized under immense pressure and heat. Whether it…

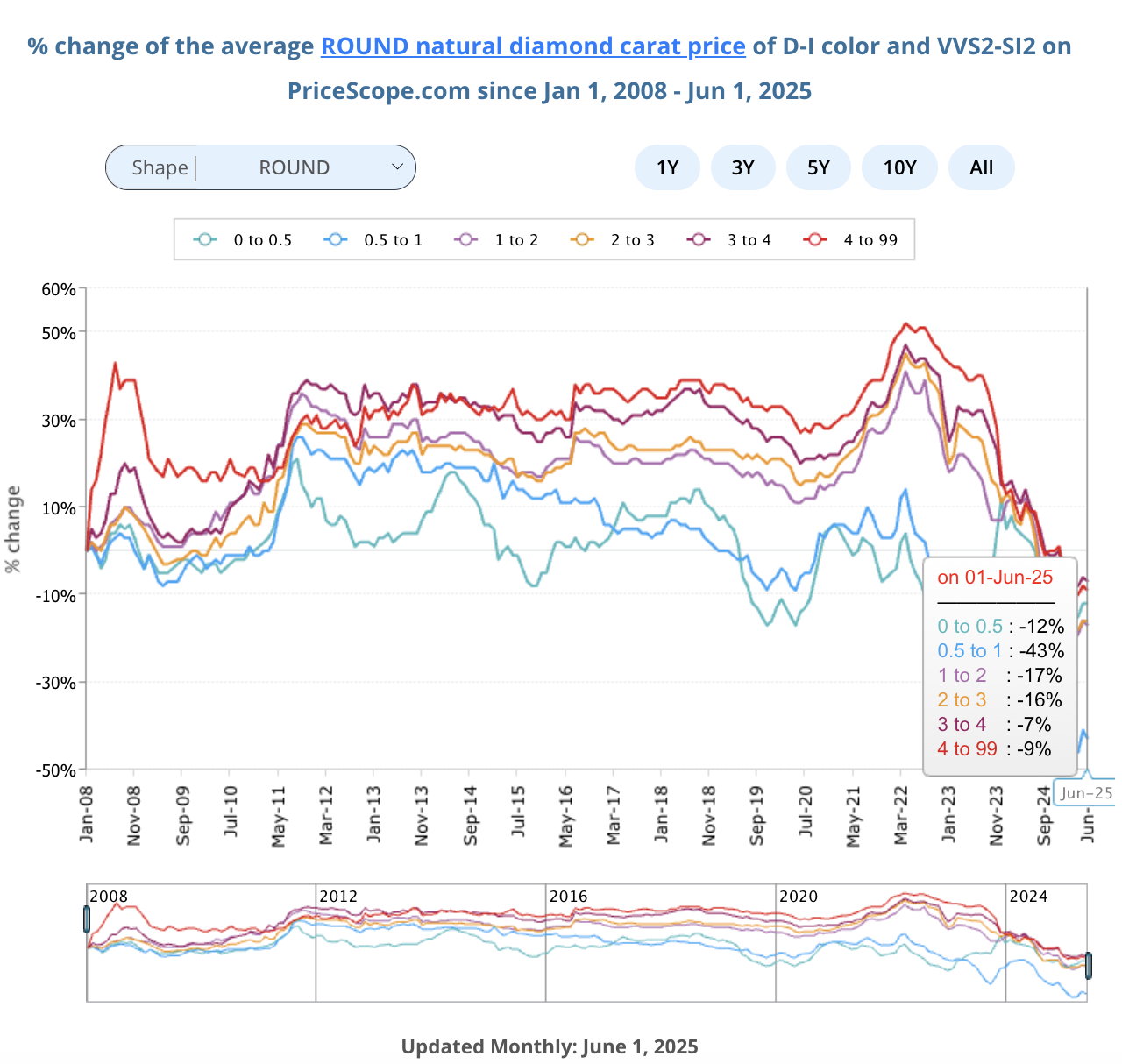

The natural diamond market in May 2025 showcased diverse pricing trends across clarity and color categories, shaped by evolving consumer preferences and intensified competition from lab-grown diamonds. This month’s insights highlight a dynamic environment, presenting both opportunities and challenges across premium, mid-range, and budget-friendly diamond grades.

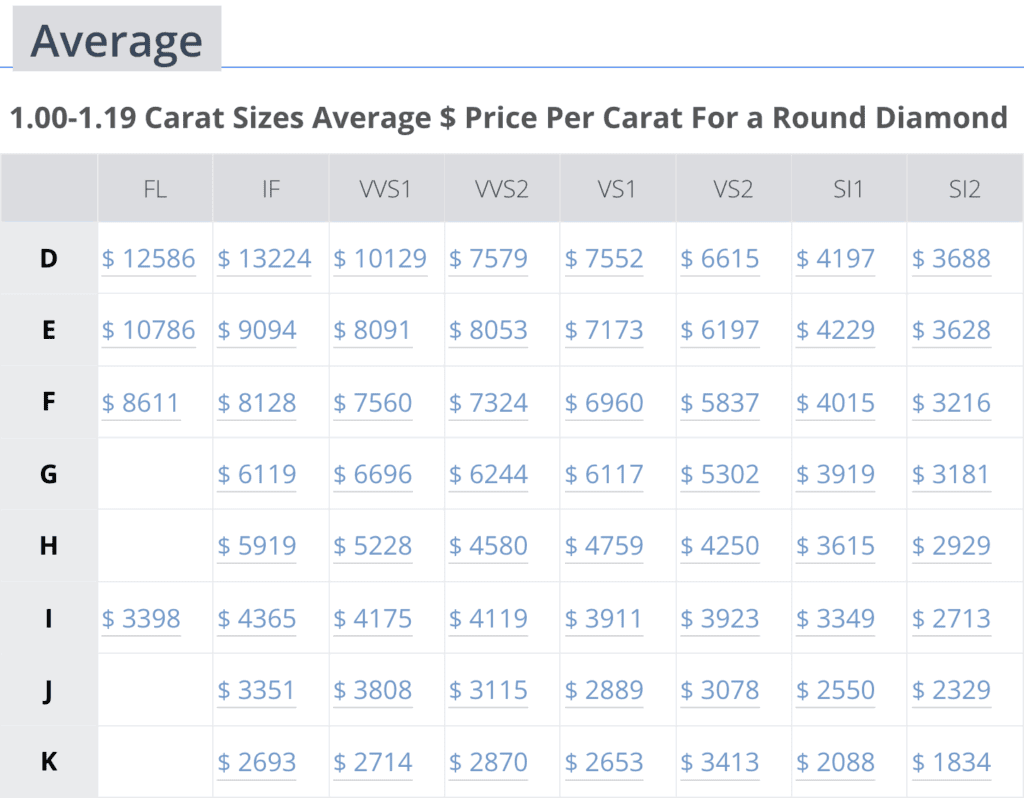

Premium diamonds experienced mixed price movements in June. D/FL clarity diamonds dipped slightly from $13,218 in May to $12,586, while D/IF clarity strengthened to $13,224 from $12,964, reflecting selective demand for internally flawless stones. E/FL clarity remained unchanged at $10,786, suggesting market stabilization. Meanwhile, F/VVS1 diamonds advanced to $8,611 from $8,539, hinting at a gradual uptick in consumer confidence in premium categories.

The mid-range segment continued to see steady interest with slight variations. H/VS1 clarity diamonds rose to $4,759 from $4,755, maintaining their attractiveness among buyers seeking quality within budget. However, F/VVS2 diamonds slipped slightly to $7,560 from $7,349, indicating nuanced shifts in preferences within this category.

Lower-grade diamonds faced mixed pressures. J/SI1 diamonds decreased slightly to $2,550 from $2,570, while K/SI2 diamonds decreased slightly to $1,834 from $1,897. I/SI1 diamonds saw a marginal rise to $3,349 from $3,251, underscoring ongoing challenges within this segment but some signs of resilience as price pressures ease.

June’s trends reveal a slight drop in the top-end D/FL category and resilience in D/IF diamonds, with mid-range diamonds holding firm. Lower-grade diamonds continue to grapple with price pressures but show tentative signs of recovery. Retailers and wholesalers can capitalize on these patterns by adapting marketing strategies and inventory mixes to meet shifting consumer needs, particularly with lab-grown competition intensifying in lower and mid-range categories.

Retail Diamond Prices Chart Updated Monthly.

Two Paths, One Diamond Not all diamonds come from the same place — but they all start the same way. Pure carbon, crystalized under immense pressure and heat. Whether it…

A Wedding Ring as Unique as Your Love Finding the right wedding ring isn’t just about diamonds or gold – it’s about finding the one that feels right. With hundreds…

So, you’re thinking about lab-grown diamonds? Smart move. They’re just as sparkly as the natural kind but usually cost less. But where do you actually go to buy them? It…

is an easy tool that analyzes the data of round diamonds and calculates a score that grades cut quality.")