Hello!

In 2011 my (now ex-husband who is very "slippery") gave me an engagement/wedding ring which included an appraisal with the following description;

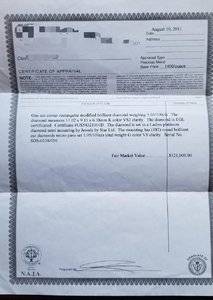

"one cut corner rectangular modified brilliant diamond weighing 5.60/100cts. The diamond measures 11.02x9.13x6.38mm K color VS2 clarity. The diamond is EGL certified. (certificate #here). The diamond is set in a Ladies platinum diamond semi mounting by Jewels by Star Ltd. The mounting has (182) round brilliant cut diamonds micro pave set 1.05/100cts total weight G color VS clarity. (serial no here)." Fair Market Value $121,000.00

The jeweler is extremely reputable in my community and services a very high end clientele. The appraisal is stamped with both "graduate of GIA" and as a "senior member of N.A.J.A" with the document having a boarder that I have seen on sights demonstrating a "legit" appraisal.

* Before you say it - as a side note, I have since had it GIA Certified and the only difference (though a big one) is that the color is really "M" *

My husband once told me that it cost over $4000 a year to add this insurance rider to our homeowner policy. Last year I visited the Jeweler about possibly purchasing the ring back. After much pressing, he showed me the file and I learned that my husband's total purchase price was for $43,000 - however, only $9000 out of pocket, the remaining balance was through an insurance claim on another ring he had that said jeweler discovered a "crack" in. The jeweler then informed me that "you don't want that appraisal" and educated me to the fact that an insurance company would only provide me with the replacement value, which would be about $45,000.

The ring is beautiful and more than I would have ever expected. I am not a diamond snob and could care less about the color. Frankly, I was wearing what most people pay for a car, on my ring finger. I didn't need to think it was the price of a condo instead and never had a reason to see the appraisal. - SO WHY ON GODS EARTH, would an appraiser/jeweler almost triple the fair market value on a ring, risking his credentials for something that does NOTHING for anyone but cost outlandish insurance premiums? What would you - or is there anything that can be - done about this practice?

In 2011 my (now ex-husband who is very "slippery") gave me an engagement/wedding ring which included an appraisal with the following description;

"one cut corner rectangular modified brilliant diamond weighing 5.60/100cts. The diamond measures 11.02x9.13x6.38mm K color VS2 clarity. The diamond is EGL certified. (certificate #here). The diamond is set in a Ladies platinum diamond semi mounting by Jewels by Star Ltd. The mounting has (182) round brilliant cut diamonds micro pave set 1.05/100cts total weight G color VS clarity. (serial no here)." Fair Market Value $121,000.00

The jeweler is extremely reputable in my community and services a very high end clientele. The appraisal is stamped with both "graduate of GIA" and as a "senior member of N.A.J.A" with the document having a boarder that I have seen on sights demonstrating a "legit" appraisal.

* Before you say it - as a side note, I have since had it GIA Certified and the only difference (though a big one) is that the color is really "M" *

My husband once told me that it cost over $4000 a year to add this insurance rider to our homeowner policy. Last year I visited the Jeweler about possibly purchasing the ring back. After much pressing, he showed me the file and I learned that my husband's total purchase price was for $43,000 - however, only $9000 out of pocket, the remaining balance was through an insurance claim on another ring he had that said jeweler discovered a "crack" in. The jeweler then informed me that "you don't want that appraisal" and educated me to the fact that an insurance company would only provide me with the replacement value, which would be about $45,000.

The ring is beautiful and more than I would have ever expected. I am not a diamond snob and could care less about the color. Frankly, I was wearing what most people pay for a car, on my ring finger. I didn't need to think it was the price of a condo instead and never had a reason to see the appraisal. - SO WHY ON GODS EARTH, would an appraiser/jeweler almost triple the fair market value on a ring, risking his credentials for something that does NOTHING for anyone but cost outlandish insurance premiums? What would you - or is there anything that can be - done about this practice?

300x240.png)